Trusts Did Not Benefit Family in £442k Inheritance Tax Case

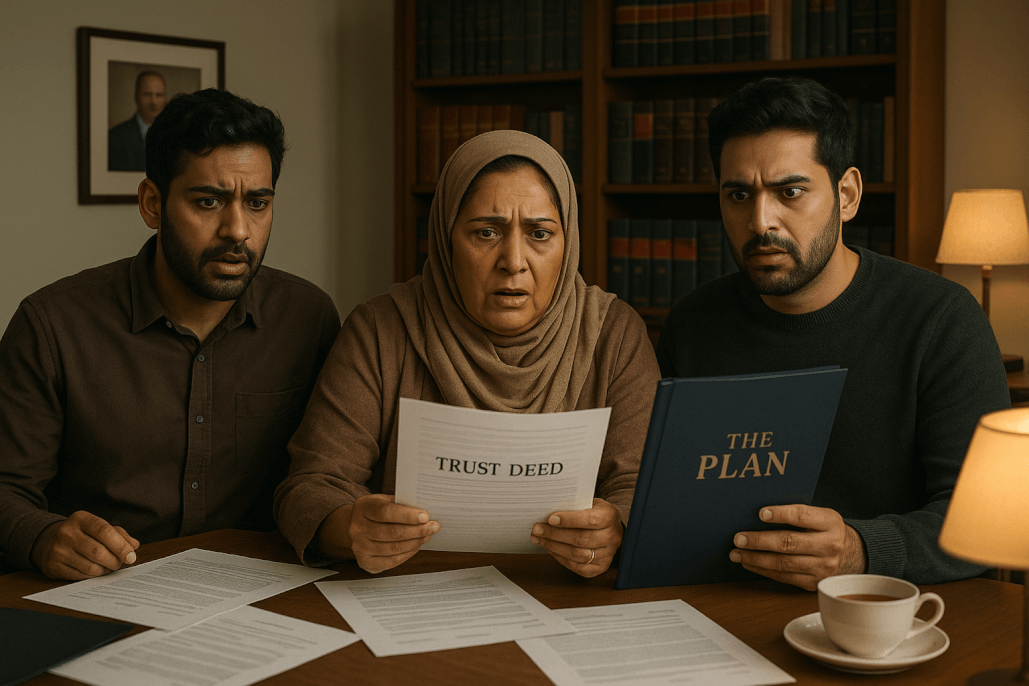

The recent case of Afsha Chugtai vs HMRC has significant implications for Inheritance Tax (IHT) legislation, particularly regarding trusts. The tribunal examined whether funds in two trusts qualified for exemption from IHT, ultimately concluding that they did not benefit the family as intended ... The 'Afsha Chugtai vs HMRC' case serves as an essential teaching moment in the realm of inheritance tax and trust law The complexities surrounding inheritance tax can often feel daunting, especially when cases revolve around the intricate nature of trusts and the stipulations of relevant legislation. A recent tribunal ruling, 'Afsha Chugtai vs HMRC [2025] UKFTT 00458 (TC)', has once again highlighted just how convoluted these matters can become. In this particular case, the late Mohammed Chugtai's estate was scrutinised, leading to a disagreement between HM Revenue and Customs (HMRC) and his daughter and executrix, Afsha Chugtai, over potential inheritance tax liabilities. At the heart of the matter was the interpretation of Section 102 of the Finance Act 1986!This pertains to gifts with a reservation of benefit. While gifts made more than seven years before death are generally exempt from Inheritance Tax, this exemption does not apply if the donor continues to enjoy the property or retains some benefit from it. This legislation was key to HMRC's argument that the trusts, designed to reduce Mr. Chugtai's chargeable estate by £442,239, were invalid due to a retained benefit. In a rather commendable move, the tribunal judges were eager to commend the legal representatives for their clear submissions. The legal battle underscored not just the intricacies of Inheritance Tax, but also the importance of how such cases are presented. For those seeking to challenge HMRC's findings, it highlights the necessity of presenting a robust case - complete with personal testimony and reliable evidence. As it relates to the case, Mr. Chugtai had established two discretionary ‘interest in possession trusts’ in February 2000, aimed at benefiting his children. While the trusts were structured to exclude the deceased from benefiting from their assets, he returned to the Caversham property to care for a child with mental health issues, occupying the property without any evidence of paying rent. In the eyes of HMRC, this was a clear indicator of | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Would you like to know more? |

If anything I've written in my blog post resonates with you and you'd like to discover more of my thoughts about this case or ensuring you maximise the benefits from a trust correctly, then do feel free to call me on 01908 774323 and let's see how I can help you. |

Share the blog love ... | |||||||||||||||||||||||

#InheritanceTax #EstatePlanning #Trusts #TaxLaw #TaxPlanning |

About Helen Beaumont ... | ||

|

More blog posts for you to enjoy ... | ||

| HMRC Taking A Good Look At Savvy Online Sellers HMRC's new data sharing initiative, which aligns with the OECD's global objective to tackle tax evasion, has been met with mixed reactions from online sellers ...... | |

| Probate: what documents do executors need to get started? What documents do executors need? In short, the papers that prove identity, assets, liabilities and family links matter most. Good records make probate application documents easier to prepare, reduce delays and help executors... | |

| How Zero-Hours Contracts are changing under new rules Zero-Hours Contracts are not being banned, but they are being tightened dramatically. The direction of travel is clearer pay, more notice, and fewer surprises for workers. UK employers should start thinking now about how they... | |

| New dividend disclosures for close company directors explained Dividend disclosures on the new SA102 boxes can feel fiddly at first, but the key point is simple. If the person is a director of one close company, the reporting follows that company, not every company in which they happen t... | |

| Why splitting a business to avoid VAT can backfire badly Splitting a business to avoid VAT may look clever, but it often isn't. HMRC can join entities together where links exist and challenge the arrangement. Consider contracts, commercial reality, and long-term costs before acting... | |

| Welcome to the summer of VAT complexity and 5% surprises This summer's VAT complexity is not just about cheaper tickets and meals. It also brings fresh admin, tricky boundaries, and significant VAT compliance work for businesses. A small saving for families, perhaps, but a big exer... | |

| Why the middle-income trap matters in the salary sacrifice cap The salary sacrifice cap sounds as though it is aimed at high earners, but the detail creates a middle-income trap for everyday savers and SMEs. Below £2,000, the system still works well; above that, NI costs, payroll pressur... | |

| Final P11D deadline for HMRC expenses and Benefits in Kind filing The P11D deadline for HMRC expenses remains important this year, but bigger changes are coming soon. Employers using the old system should file on time, while others should start preparing for payroll reporting of Benefits in... | |

Other bloggers you may like ... | ||

| Remote working gave people freedom, but less human contact Posted by Steffi Lewis on https://www.yourping.uk Remote work has transformed modern working life. For many, it has brought flexibility, reduced commuting costs and a better work-life balance. The fre ... | |

| Do I actually still work? Absolutely, I just work differently Posted by Davina Farrer on https://blog.joindavina.co.uk One question I get asked quite a lot is, 'Do you actually still work?' I always smile because I can see why people ask, but I do, in fact, work incred ... | |

| Why you should only use AI as a research tool, not the final word Posted by Pritesh Ganatra on https://blog.btsuk.net Use AI as a research tool to spark ideas and speed up reading. Then verify, compare sources, and keep judgment yours. It's guidance, not gospel ... ... | |

| 10 reasons YourPCM is the small business CRM you'll actually use Posted by Steffi Lewis on https://www.yourpcm.uk Choosing a CRM can feel like a big decision, especially when so many systems promise everything but end up being overly complicated, expensive, or sim ... | |